A government consultation on simplifying R&D Tax Relief into a single scheme closed on 13th March 2023, and whilst views have been invited, it feels very much like a “done deal” that a new merged scheme based on the current RDEC scheme will emerge.

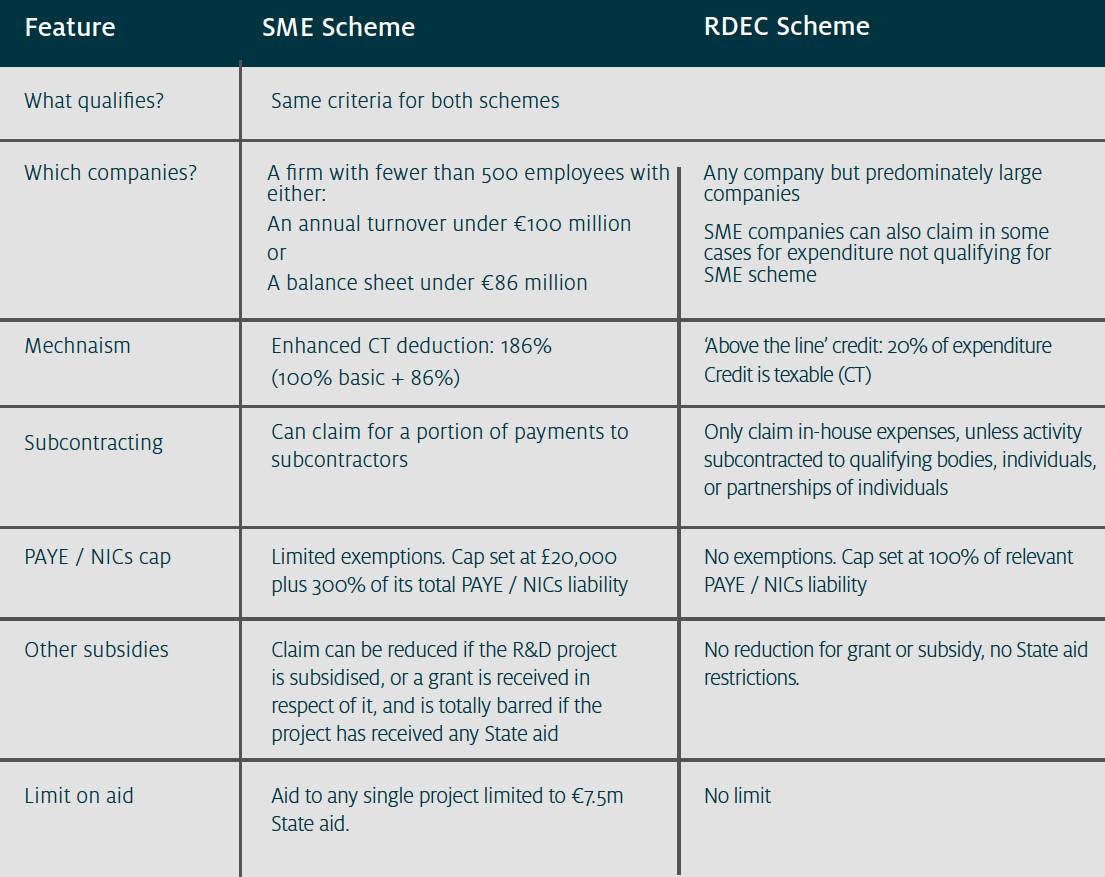

The small and medium enterprise (SME) scheme was introduced in 2000 followed in 2002 by a scheme for large companies. Following consultation in 2011 RDEC was introduced for large companies and SMEs ineligible for the SME scheme. The large company scheme was phased out after a transition period from April 2013 so that from 2016 all large companies claimed the new Research and Development (R&D) expenditure credit (RDEC).

Following the changes announced in the last Autumn Statement the generosities of the two R&D tax schemes are broadly aligned from April 2023 and Government feels there is now scope to simplify the system and merge the two schemes.

The Chancellor’s Autumn Budget announced support for R&D through the tax reliefs will continue to increase, from £6.7 billion in 2020-21 to over £9 billion in 2027-28 – but in a way that is intended “to ensure better value for the taxpayer”.

So, what does that really mean?

- We’re coming for the fraudsters and “cowboys” who submit inaccurate claims.

- Credits are going to be directed to those businesses who really prove they are reinvesting in new innovation to drive growth.

Problems

In the HMRC annual report and accounts: 2021 to 2022 the estimated level of error and fraud within Corporation Tax R&D reliefs was £469 million or 4.9% of related expenditure in 2021-22. This comprises £430 million (7.3%) in the SME scheme and £39 million (1.1%) in the RDEC scheme…. so it is clear where the bulk of the problem lays. The estimate is based on outcomes of compliance cases completed in 2020-21 and 2021-22 and assumptions on error and fraud within unreviewed cases. The rate is higher than the 2020-2021 estimate and reflects improvements in HMRC’s “risk identification process” to better identify non-compliance.

Steps announced in 2021 have already seen a specialist HMRC R&D team focused on SME compliance more than double in size but the full measures to combat error and fraud are due to be implemented from April 2023. Measures include requiring all claims to be:

- Made digitally.

- Accompanied by a technical report.

- Supported by a named officer of the company.

- Transparent about any agent associated with the claim.

In addition, HMRC is therefore currently conducting a mandatory random enquiry programme to build a better understanding of error and fraud……so companies who have not been well advised on their R&D claims or submitted “lazy” claims themselves are never more likely to face problems.

Opportunity for increased profits

But there is certainly good news too!

Alongside the RDEC rate increasing from 13% to 20% from April 2023, there are other changes that potentially increase returns for businesses conducting appropriate activities:

- All cloud computing costs associated with R&D, including storage, will qualify for relief.

- Where it is necessary for the R&D to take place overseas, expenditure on overseas R&D activities could still qualify where there are:

- material factors such as geography, environment, population, or other conditions that are not present in the UK and are required for the research – for example, deep ocean research,

- regulatory or other legal requirements that activities must take place outside of the UK – for example, clinical trials.

- To support the growing volume of R&D underpinned by mathematical advances, the definition of R&D for tax is expanded by clarifying that pure mathematics is a qualifying cost.

Most importantly, HMRC are committed to rewarding those businesses who truly reinvest the proceeds of their R&DTC to support further innovation as a driver for growth.

As such, the additional £2Billion of resources pledged annually over the next 5 years will be shared amongst fewer businesses who can evidence innovation via professional, detailed technical reports that provide true insight into the claimants’ activities.

Ironically, this comes at a time when specialist professional R&D resources made available to clients from the traditional “Big 4” accounting firms has never been more scarce – perhaps as the greater technical and scientific “burden of proof” is outweighing the “pure accounting” aspects of presenting claims.

Avoid problems. Seize the upside and profit from the new dawn.

To ensure your business is neither missing out on legitimately maximising its R&D Tax Credit, nor inadvertently submitting an inaccurate, non-compliant claim as the R&D landscape changes, the right advice and consultation is essential.

ERA work exclusively with a small panel of specialist R&D Tax Credit specialists, not only embracing the “new dawn”, but actively driving change through close consultation with HMRC. Our partners are carefully vetted and monitored to ensure clients receive the value through insight we demand.

Contact your usual ERA contact or Paul Gravatt directly on 07860 780 770, pgravatt@eragroup.com who will be delighted to facilitate a review of your circumstances and provide specialist insight advice.